Dear Clients and Friends,

As always, we begin a new year extremely grateful for the gift of life, health, family and the joy of living in the beautiful Pacific Northwest.

STRONG FOURTH QUARTER FOR STOCKS

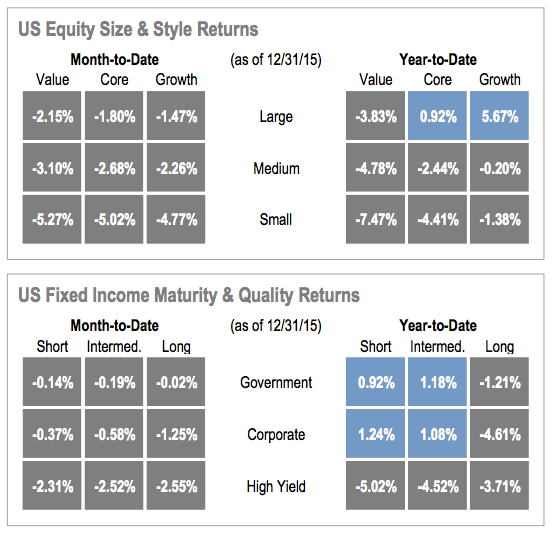

After a very difficult summer for stock markets both here and abroad, we were pleased to see a nice bounce back in the equity markets during the 4th quarter, erasing most of the earlier losses for stocks through the 3rd Quarter of the year, with the S&P500 finishing 2015 up 1.3%. The S&P500 gains in 2015 were incredibly lopsided, with the top 10 stocks in the index up an average of 71% and the remaining 490 stocks collectively down nearly 4.6%. The chart below shows this discrepancy very clearly and highlights why many investors with a “diversified portfolio” under performed the index in 2015.

While all global stock markets showed strength during the 4th quarter, most foreign stocks finished the year (once again) in negative territory with the strongest losses coming from emerging markets with the MSCI EM index down 14.92% for the year.

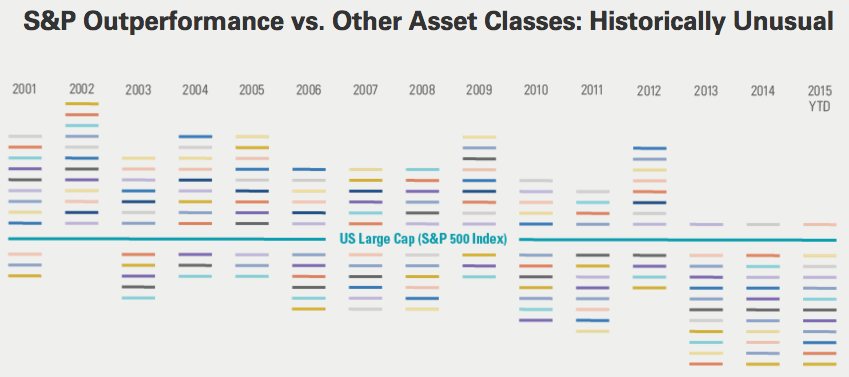

This is the 3rd straight year that the US markets as defined by the S&P500 have outperformed their global competitors as well as almost all other asset classes. The well-espoused virtue of diversification (not having all your eggs in one basket) has simply not held true over the past 3 years, and advisors across the board have experienced this as demonstrated by the chart below.

The absolute truth is that making money in the stock market was extremely challenging for financial advisors last year who believe in diversification via asset allocation, and our winning investments in one sector of the market were offset by losses in other sectors. Even the Oracle of Omaha famed investor Warren Buffett’s Berkshire Hathaway was down over 12% last year.

While all global stock markets showed strength during the 4th quarter, most foreign stocks finished the year (once again) in negative territory with the strongest losses coming from emerging markets with the MSCI EM index down 14.92% for the year.

CHINA’S ECONOMY IS IN TRANSITION

Markets around the world are sharply lower so far in 2016, in response to the belief that China’s market is cooling, as evidenced by a slight decline in manufacturing for the month of December. China is viewed as “the world’s factory,” rising to prominence by selling stuff mostly to other nations. Today China is evolving into a consumer society more like the US and much of Europe, and so it is to be expected that this transition from predominantly manufacturing to more of a consumer driven society will impact the economic landscape in China. In the journey from a “closed market” to a more open and free economy, we can expect that there will be bumps and false starts along the way.

The evidence of China’s burgeoning middle class is supported by the fact that China-based consumers shopping U.S. brands online over the holiday season in 2015 increased an impressive eightfold versus 2014, according to Ant Financial Services Group’s Alipay. China’s service economy grew 8.4% in the first nine months of 2015, whereas manufacturing was only up 6%. This transition in China’s economy is highlighted by the graph below. With China contributing 39% of Global GDP growth in 2015, we should expect that market volatility will accompany the changes that China is experiencing in their economy. While not without volatility along the way, a more open market economy should bode well for China and those companies doing business in China.

WHAT IMPACT WILL RISING RATES HAVE IN 2016?

As developed economies enter a seventh year of expansion, the velocity of growth continues to be underwhelming, yet resilient. Against this backdrop, we don’t expect to see the Federal Reserve being aggressive in their rate hikes, and feel that a well-diversified fixed income allocation still plays an important role in a client’s portfolio, particularly for retired or more conservative clients.

As opposed to simply a stock/bond and possibly real estate portfolio, we are also currently doing our due diligence on some very interesting institutional/ultra high net worth separate account managers (SMA) that we will have access to for our TD Ameritrade clients at the beginning of the second quarter. Some of these managers run total return portfolios that focuses on a tight range of returns through all market conditions, making their management a very attractive option to some of the more traditional fixed income only managers out there. We are excited to share more about this as we approach the second quarter.

We believe that real estate should continue to see growth in 2016 despite a modest rise in interest rates, and those clients currently with exposure to real estate private placements have enjoyed the benefits of the diversification and non-correlation to the stock markets that this asset class typically exhibits.

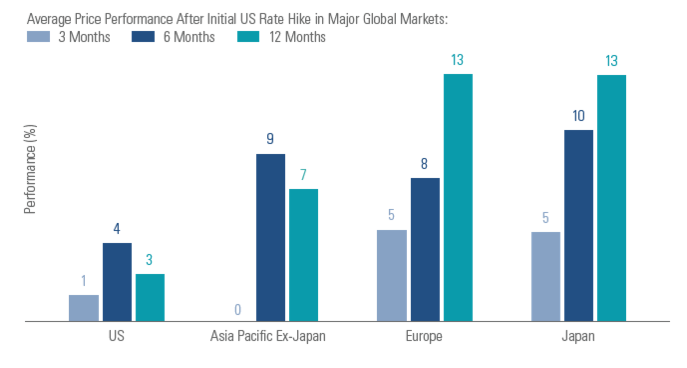

In support of our belief in some allocation to foreign markets, the chart below highlights how these markets have done historically when the US has begun to raise interest rates.

2016 INVESTMENT OUTLOOK

With US equities being close to fully valued, returns will need to come from earnings growth, fueled by increasing consumer confidence and spending. While the economy is in a later phase of expansion, we expect modest growth this year, and see the odds of a recession as very low. Growth abroad should potentially be even stronger than here at home.

We like Europe in 2016, both from a valuation standpoint as well as the fact that growth seems to be coming from increasing consumer confidence that leads to spending.

We believe that low oil prices will continue to benefit consumers in 2016, and also expect to see continued strength in the housing markets this year.

The US dollar looks set to experience another year of strength against global currencies, so if you’ve been putting off that trip to Europe, now might be the time to reconsider it.

We are in the midst of some exciting developments here at the firm, and are particularly excited by some new investment options that will expand even further our ability to provide you with world-class money managers.

While the advisor community has generally trailed the performance of the S&P500 over the past few years, thanks to issues discussed in this commentary, we believe the case for diversification both here at home and abroad is growing increasingly more attractive. While we would never bet against the US economy, valuations for stock markets in Europe and other parts of the developed world are simply less expensive than here in the US, in addition to a resurgence of consumer confidence and spending in these regions. The US is still the largest economy on the planet and in times of uncertainty will always be the relative safe haven; and we will not lose sight of this reality.

We understand that these are challenging times for investors, and while it would be easy to get caught up in the day to day gyrations of the stock markets here and abroad, we once again want to encourage a long-term view. Studies have shown how important it is to not miss those “best days” in the market. And while it’s tempting to want to step out of the markets, timing the markets is not a recipe for long-term success.

We look forward to concluding our research and analysis over the next few months and believe that our time and efforts may well lead to some exciting new tools for you, our clients.

As always, we appreciate your confidence and trust, and invite your thoughts or questions.

YOUR PINNACLE WEALTH ADVISORY TEAM